- Like

- SHARE

- Digg

- Del

- Tumblr

- VKontakte

- Flattr

- Buffer

- Love This

- Save

- Odnoklassniki

- Meneame

- Blogger

- Amazon

- Yahoo Mail

- Gmail

- AOL

- Newsvine

- HackerNews

- Evernote

- MySpace

- Mail.ru

- Viadeo

- Line

- Comments

- Yummly

- SMS

- Viber

- Telegram

- JOIN

- Skype

- Facebook Messenger

- Kakao

- LiveJournal

- Yammer

- Edgar

- Fintel

- Mix

- Instapaper

- Copy Link

getty

A car insurance, also called motor insurance, offers financial protection to your vehicle against accidents, burglary, theft, fire, natural calamities such as a storm or, earthquake, and other unforeseen circumstances.

Every car that runs on Indian roads is expected to have a basic third-party insurance policy made mandatory by the Indian federal government under the Motor Vehicles Act, 1988.

The basics of how a car insurance works is that the car owner pays premiums for an insurance cover to a motor insurance company, which in return pays claims for any damages caused at the time of an untoward incident. The difference lies in the many offerings that car insurance companies have to meet varied requirements.

Let’s look at how you can get your car insurance policy to tick the right boxes for your needs.

An Insurance Cover To Meet Your Requirement

There are three types of car insurance available:

Third-Party Liability Insurance Cover

This cover is the basic cover that every car owner compulsorily needs to have in India. It offers basic protection via its features such as:

- It is meant to protect a third-party that is at risk of injury or damage while you are driving.

- If your vehicle hits someone else, their car or their property, the third-party insurance cover will provide financial assistance to the person to set their damages right.

- This insurance cover does not cover damages or injuries caused to your vehicle. Thus, at the time of an accident, you don’t enjoy financial protection for yourself.

Standalone Own Damage Insurance Cover

This cover is to insure your car against damages in case of an accident, natural calamity or theft, among others.

Till September 2019, own damage insurance coverage was bundled with the third-party liability insurance policy mandatory under Indian laws. If you have bought your car after September 2018, you can buy a standalone own car damage insurance plan separately.

Some of its features include:

- This coverage is for the owner-driver of the vehicle such that:

(a) the owner-driver is the registered owner of the vehicle insured.

(b) the owner-driver is the insured named in this policy.

(c ) the owner-driver holds an effective driving license.

- The purchase and renewal of your own damage cover in an existing third-party insurance cover is now independent and optional.

Comprehensive Insurance Cover

This is an extensive motor insurance plan that covers the insured person against both, own damages and third-party liabilities.

Among important features of comprehensive insurance cover are:

- It offers protection in cases like natural disasters, fire, falling objects, theft, civil disturbances and vandalism.

- It allows you to add features to enhance the scope of your insurance cover via add-ons.

- The policy has the option of a No Claims Bonus where if you don’t make any claim during the tenure of the policy, you can avail a bonus or a discount on your next premium schedule.

All the three types of insurance covers available for an Indian consumer don’t provide protection against damages caused due to:

- Damage to the car when the driver is driving without a valid driving license.

- Damage to the car when the driver is driving under the influence of alcohol or other intoxicants.

- Damage outside the geographical scope of the policy.

- Damage to tyres and tubes unless the vehicle is damaged at the same time in which case the liability of the company shall be limited to 50% of the cost of replacement.

- General wear and tear due to ageing.

- Mechanical or electrical breakdown.

- Failure or breakages.

Add-ons To Enhance Your Insurance Cover

Add-ons refer to additional coverages that offer an extra layer of insurance for a premium. They can be clubbed with a comprehensive insurance cover and are not applicable for a basic third-party liability cover.

A suitable way to choose your add-ons is:

(a) be aware

(b) calculate your own needs

Popular add-ons include:

Zero Depreciation

There are certain car parts that depreciate with time. Any claims on an insured vehicle are settled keeping in mind the depreciation value of these car parts usually made of plastic, rubber, glass and fibre.

What a zero depreciation add-on does is it helps you claim costs associated with car parts that depreciate with time.

This add-on is good for people who live or work in areas where there is no proper parking and mischievous personnel may damage the car’s glass panes. It is particularly useful if you drive in an accident-prone area.

Return to Invoice Cover (RTI)

This add-on helps you cover the gap between the insured declared value (IDV) and the invoice value of your car along with the registration and other applicable taxes.

This is most useful in case of total loss when your car is damaged beyond repair or is stolen, in which case, the car insurance company pays the purchase price of your car.

This one is suitable for those who drive on accident-prone highways or don’t have a proper parking space at their workplace or home.

Personal Accidental Cover (PA)

This add-on protects you, the insurance policy holder, and the passengers in the car against the risk of physical disability or death due to an accident.

When you buy this add-on, a stipulated insurance claim is paid to the nominee of the insurance policy holder, who is the owner-driver of the insured vehicle, in case of death or permanent disability. The passengers in the car will also receive financial protection in case of injury or death.

The add-on includes features such as:

- Covers medical treatment costs for passengers in case of an accident.

- Provides financial assistance in case of the death of passengers.

- Provides disability liability cover to passengers of the insured vehicle.

- Avoid legal hassles if the insured vehicle is a commercial passenger car.

You could choose to buy any of the two types of PA cover:

Unnamed Passenger Cover: This cover provides for financial assistance for everyone sitting in the car.

Paid Driver Cover: This provides protection to a driver apart from the owner who is the policyholder. This cover is for those who often travel in a chauffeur-driven car.

Engine Protection

This cover provides the full cost for repair of a damaged engine, which could happen via anything from leaked lubricant to fire.

This policy is helpful for people living in flood-prone areas and areas that receive high rainfall and are prone to waterlogging.

Consumables Cover

This add-on insures your car against all car items that are subject to wear and tear. For example, nuts, bolts, screws, washers, brake oil, engine oil, gearbox oil, power steering oil, radiator among others.

Your basic car insurance policy does not cover damage to any consumables and that makes this cover useful.

This cover is suitable for those who have long driving schedules on a daily basis or have to drive in rough terrains.

Roadside Assistance

This cover helps you get help if your car breaks down in the middle of your journey. It is useful for multiple small yet essential services relating to a car breakdown such as:

- Minor repairs

- Towing service

- Flat tyres

- Sudden battery breakdown

- Delivery of fuel

- Fetching spare keys

Have Your Checklist Ready

Before finalizing your car insurance policy, you must check these factors that are significant deciding factors when finalizing a cover:

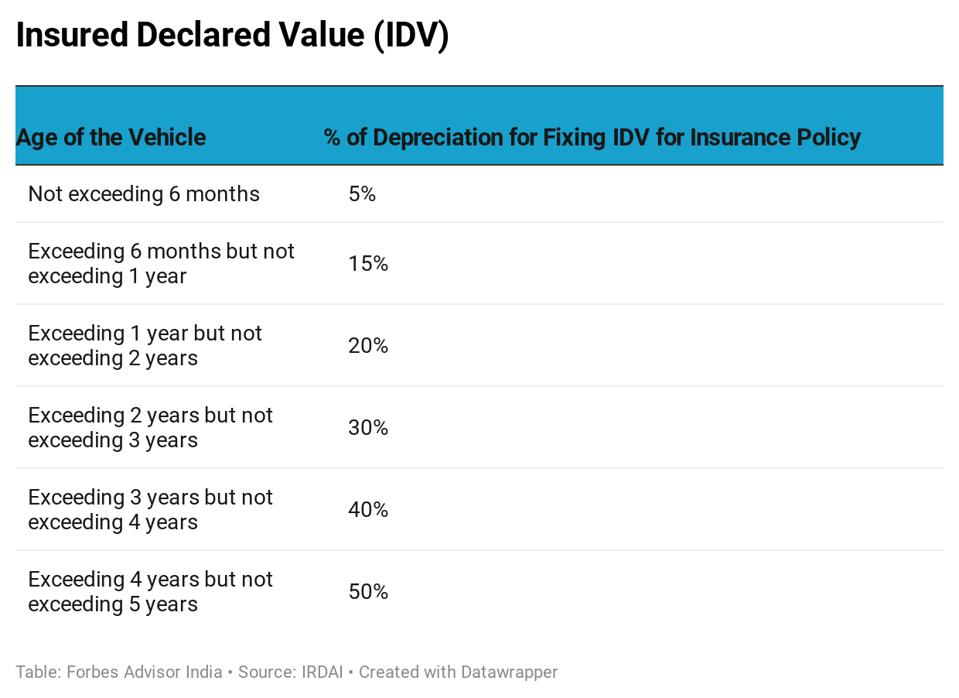

Insured Declared Value (IDV)

The IDV of the vehicle is the sum assured in case of theft or damages to your car beyond repair.

It is fixed at the commencement of each policy period for the insured vehicle on the basis of the market price or the manufacturer’s listed selling price of the brand and model of the vehicle insured at the beginning of the insurance plan or the renewal plan.

It is adjusted for depreciation and impacts the premium you pay for your insurance policy. Higher the IDV, more the premium and more the coverage.

The insured vehicle is treated as constructive total loss if the aggregate cost of retrieval or repair of the vehicle exceeds 75% of the IDV of the vehicle. Damages below 75% of the IDV of the vehicle fall in the total loss category.

When a claim is made on account of total loss of the insured vehicle, the following depreciation rate is considered at the time of settlement.

When a claim is made on account of total loss of the insured vehicle, the following depreciation … [+] rate is considered at the time of settlement.

Forbes Advisor India

IDV of vehicles beyond 5 years of age and of obsolete models of the vehicles is determined upon mutual understanding between the insurance company and the insured claimant.

NCB (No Claims Bonus)

NCB is the incentive or reward you get for not raising any claims through the tenure of your policy.

A beneficial car insurance policy will have a high no claims bonus, which is often offered as a percentage of the discount you may receive on renewals of your car insurance policy.

For every year you don’t make a claim, your bonus percentage increases.

Voluntary Deductible/Excess Fee

This refers to the voluntary contribution you commit to make in case a claim is raised at the time of prospective damage.

This amount, which is voluntarily agreed upon by the policyholder, is set at the time of buying or renewing a policy.

For example, if the voluntary deductible is set at INR 5000 and a claim is raised for damages worth INR 40,000, the insurance company is liable to meet INR 35,000 in claims while the remaining amount is paid for by the policyholder.

In cases where the voluntary deductible is lower than claim, the insurance company has no liability to make any payments. For example, if the claim is of INR 3000 and the voluntary deductible set at the commencement of the policy is INR 5000, the company will not pay anything rather the policyholder will take care of the expense.

Some points to note are:

- You need to pay the voluntary deductible every time you make a claim. It’s not a one-time or an annual activity.

- You need to carefully check the voluntary deductible you are signing up for at the time of buying the policy.

- If you have a high amount as a voluntary deductible then you may be able to get your insurance company to agree on a discount in your policy premium for the next year if you continue with the same insurance company.

Cashless Car Insurance Facility

As a part of this facility, insurance companies offer a network of authorized garages where you can get your car repaired without paying any cash.

When selecting a car insurance policy, it may be beneficial for you to select an insurance provider that provides this facility to make your insurance experience smoother.

Consumers must note the list of claims that can be made to their insurance companies before visiting a cashless insurance facility. Some examples of common claims that don’t feature in general policies include:

- Depreciation of certain car parts: – a cashless insurance facility may let you get your car repaired without raising a bill if all your claims find mention in your insurance policy. But you may need to pay for the depreciation of the car parts.

- Water in the engine: – you’ll need an engine repair add-on to get your engine corrected. If you don’t have the add-on, you may need to pay a sum at the cashless insurance facility.

Bottom Line

There are many intricacies relating to a car insurance cover in India. While self-awareness and learning about all aspects of your rights as a policyholder are most important, the first step to sign up for a suitable car insurance policy is to identify your needs.

Digitization of information on insurance has also made it easier for consumers to compare policies and choose the best suited for them. Diligent research can ensure you invest the right amount of money to insure yourself.